Aether Industries

Growing CEM contracts & steady LSM demand

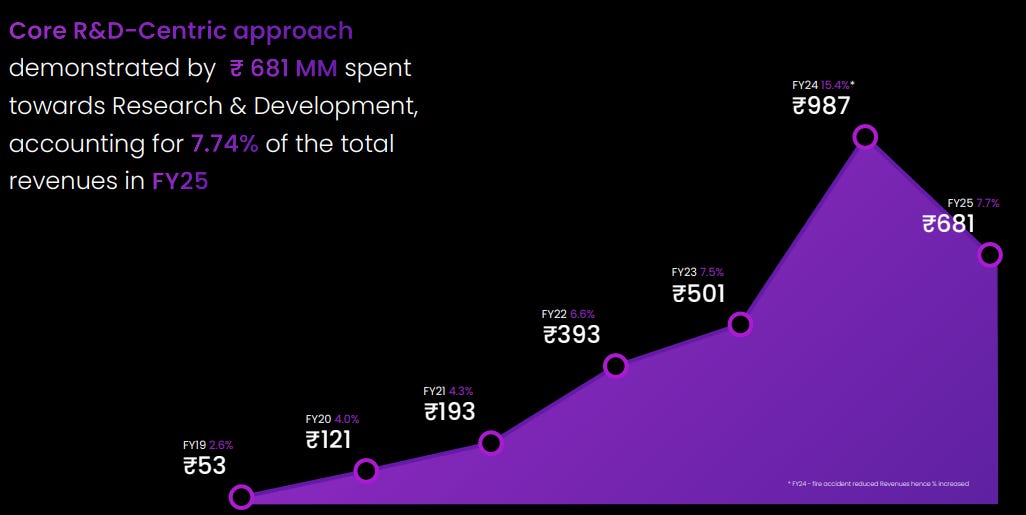

Start with the part which makes this company a bit different from others ie R&D

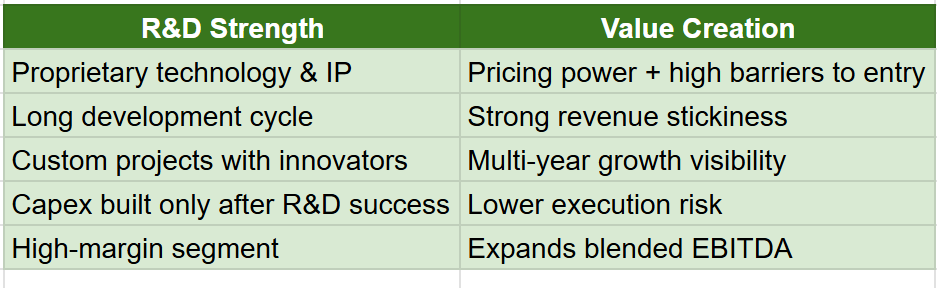

Key R&D Themes

Deep chemistry capabilities – process chemistry & scale-up strengths rather than discovery.

Strong pipeline conversion rate – high success from lab → pilot → commercial.

Custom Synthesis & Contract Manufacturing (CEM) focus as a core R&D monetization engine.

Multi-step complex chemistries creating high switching cost for customers.

R&D-led margin profile – premium pricing due to proprietary processes.

Customer-linked R&D engagements with long visibility & potential annuity revenues.

Specialization in niche chemistries – photochlorination, hydrogenation, ethoxylation, advanced polymers, etc.

New product pipeline feeding future revenue streams.

Application-centric R&D for end industries like pharma, agro, polymers & material science.

Technology scale-up as differentiator – ability to convert gram-scale chemistry into multi-MT production.

Why R&D is Critical to Aether’s Thesis

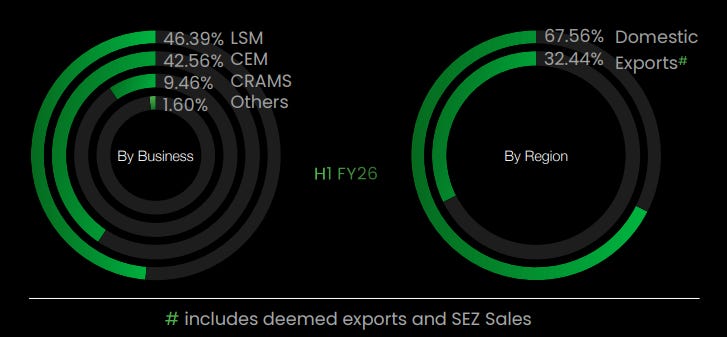

Aether’s revenue mainly comes from its three business divisions such as largescale manufacturing, CRAMS, and contract/exclusive manufacturing. Out of these three business divisions, CRAMS has the highest EBITDA margin of 70%, contract manufacturing’s EBITDA margin is around 32% and large-scale manufacturing has the lowest margin of around 25-28%

After trading at lofty valuations above 100x earnings, the P/E multiple has normalised to nearly 50x. With major capex projects set to turn productive, the business may enter a high-growth phase by FY27, potentially triggering a rerating.

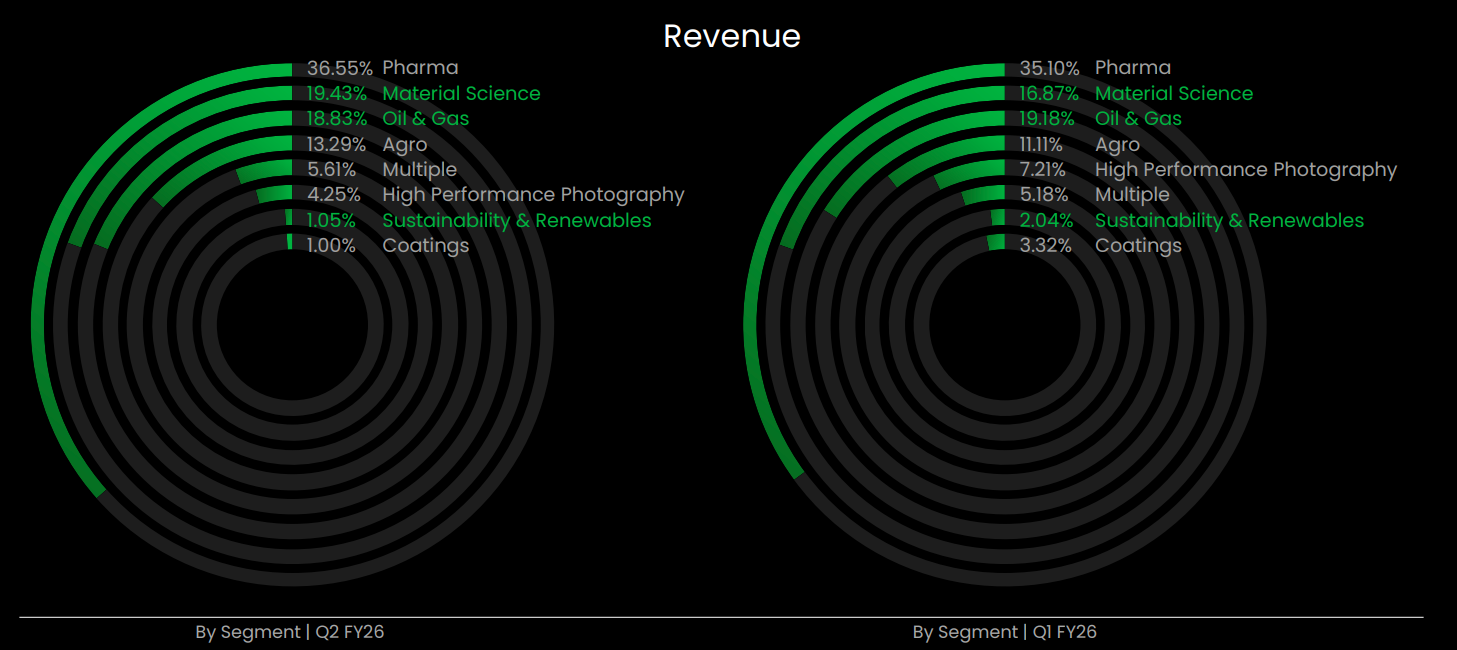

Segmental breakup ( By end user industry)

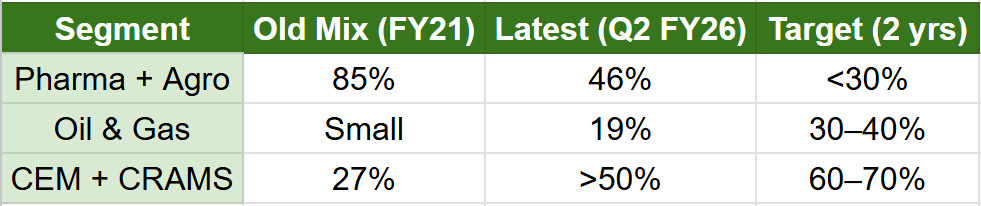

Aether is moving from “chemical intermediates for pharma & agro” → to

High-margin engineered chemical solutions for

🔹 Oil & Gas

🔹 High performance polymers

🔹 Electronic & material science applications

🔹 Global contract manufacturing

For the first time, CEM has contributed more than the LSM business vertical and CRAMS and CEM combined have contributed more than 50% of the sales.” Management goal: “CRAMS and CEM together will contribute 60%-70% of the sales in the next two years period.”

CEM

Long-term exclusive contracts where Aether is often the sole supplier.

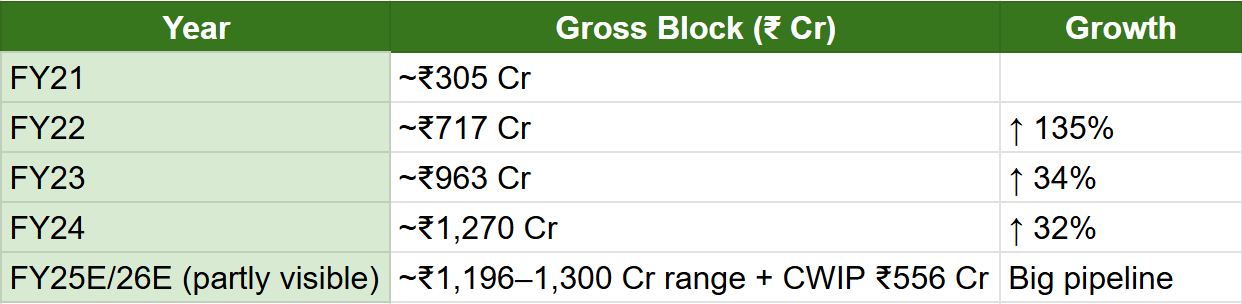

For capex-intensive businesses like Aether, gross block growth today = revenue growth tomorrow.

Gross Block Trend from the Data Provided

CWIP (Capital Work In Progress)

Aether is clearly front-loading capex aggressively. Capex growth far exceeds revenue growth so far, meaning a surge in revenue is yet to be realized.

Aether claims 2x asset turnover

Current revenues: ~₹850–1,100 Cr range

Fixed asset block potentially usable soon: ₹1,800 Cr+ (Gross block + CWIP getting capitalized)

Potential achievable revenue at 2x turnover: ₹3,600–₹4,000 Cr

Compared to FY25 revenue of ₹850–1,100 Cr → 4x scaling runway

Bull Case Interpretation

Management building for future scale, not near-term optics

Revenue & profitability will lag capex → inflection when plants start production

Capex discipline suggests visibility of long-term customer commitments

Risk View

If demand or ramp-up is delayed, returns on capex can lag → temporary ROE compression

Capital-intensive + fire incident history → execution monitoring is essential

Aether’s rapidly increasing gross block + very high CWIP indicates the company is entering a capacity monetization phase.

We are at the point where:

Capex cycle is peaking

Revenue scaling cycle is about to begin

This echoes the thesis:

Aether is transitioning from a pharma/agro-dependent intermediate maker to a global specialty chemical innovator — powered by long-term contracts, demand-led capex and export growth

If execution stays on track, medium-term returns may compound significantly as:

Capex productivity → higher asset-turnover

Mix shift → higher EBITDA margin

Earnings catch up → rising ROE from 7.8% to projected 14%

Few things to get some knowledge upon for next set of points i will try to cover.

Life sciences: chemicals used by pharma, agrochemicals, biotech, medical devices

Non-life sciences: everything else — industrial chemicals, performance materials, oil & gas, electronics

Material sciences: a subset of non-life sciences focused on materials (plastics, polymers, composites, additives) used in high-end applications

Now that out of the way.

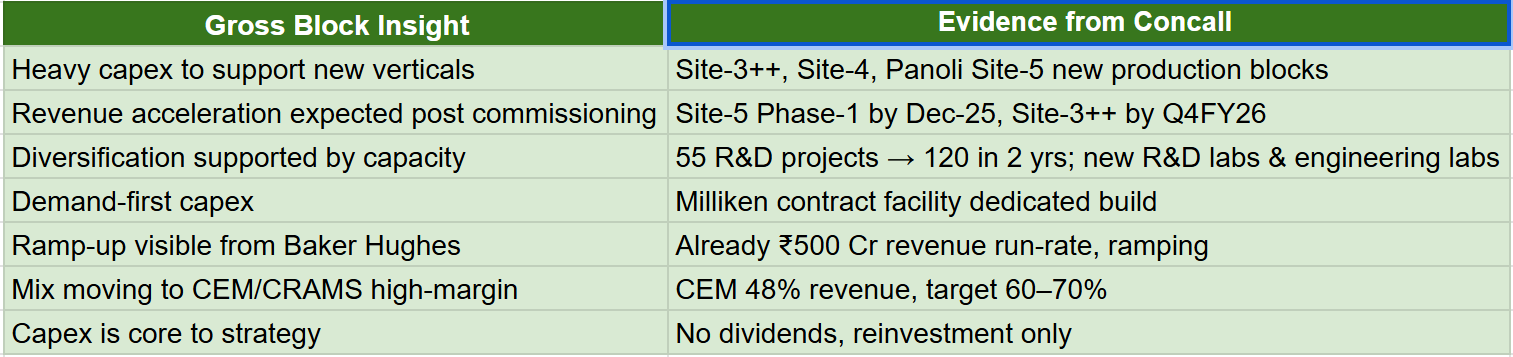

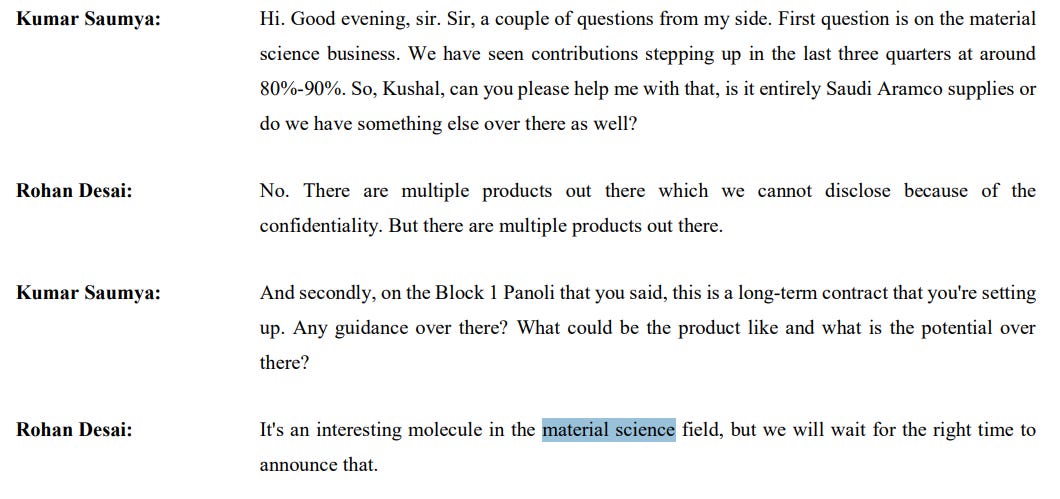

Site-3++ represents a strategic milestone, now entirely dedicated to an contract / exclusive manufacturing for a leading global material science company — a project nurtured over four years from laboratory development to full-scale commercial production

source : AR 2025

source : Concall Q2FY26

source : Concall Q1FY26

Guidances given by Aether Industries Ltd. in the Q2 FY26 concall:

EBITDA margin: Sustained around 30% (“30% margin is surely sustainable”).

PAT margin: Guided around 19–20% in the medium term (despite mix shift to higher-value segments) due to rising depreciation & finance costs.

Growth trajectory: Comfortable with ~25% growth going forward for revenue.

Mix shift: Expecting CRAMS + CEM together to contribute 60–70% of sales over the next two years.

Working capital: Targeting to bring ~140 days working capital cycle in FY27 (from ~149 days at Sep-30-25).

Asset turns: Company-level target of 1.5×–1.75× on gross block once the new capacity stabilises.

Capex funding: No further equity raise planned for next 5-7 years; growth via internal accruals + debt.

Commissioning timelines: Site-3++ (Milliken) in Q4 FY26; first two production blocks of Site-5 by start of Q4 FY26 (or Dec-25) with meaningful ramp from FY27.

Very good summary. Didn’t realise you are also tracking!